Advanced Packaging Market Size and Growth

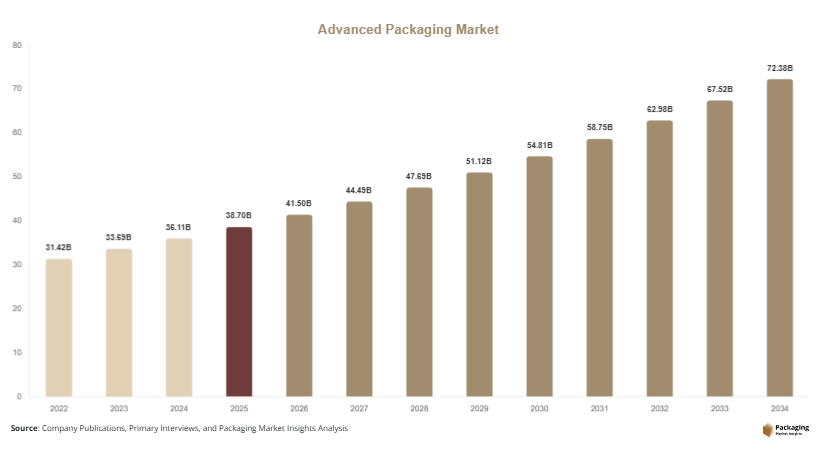

The global advanced packaging market was valued at USD 38.7 billion in 2025 and is projected to reach USD 72.4 billion by 2034, expanding at a CAGR of 7.2% during the forecast period from 2025 to 2034. The market reached an estimated value of USD 41.5 billion in 2026. The market is witnessing strong growth due to increasing demand for high-performance semiconductor packaging solutions across consumer electronics, automotive electronics, telecommunications, healthcare devices, and artificial intelligence infrastructure. Advanced packaging technologies improve chip performance, reduce power consumption, enhance thermal management, and support miniaturization requirements in next-generation electronic devices.

The growing adoption of 5G-enabled smartphones, AI accelerators, high-performance computing systems, and electric vehicles is significantly increasing the need for compact and efficient semiconductor packaging technologies. Manufacturers are increasingly investing in fan-out wafer-level packaging, 2.5D and 3D IC packaging, system-in-package solutions, and flip-chip technologies to support rising processing requirements in modern digital applications. Demand for wearable electronics and Internet of Things devices is also accelerating innovation in lightweight and compact packaging architectures.

Key Market Highlights

- Asia Pacific dominated the market with a 41.8% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.8%.

- Flip-chip packaging led the type segment with a 33.6% share.

- Organic substrates dominated the material segment with a 48.2% share.

- Consumer electronics applications led the segment with 44.9% share.

- The US remained the dominant country with a market size of USD 7.6 billion in 2025 and USD 8.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Chiplet-Based Semiconductor Architectures

The increasing adoption of chiplet-based semiconductor architectures is emerging as a major trend in the advanced packaging market. Semiconductor manufacturers are shifting from monolithic chip designs toward modular chiplet integration to improve processing efficiency, scalability, and manufacturing flexibility. Advanced packaging technologies such as 2.5D and 3D IC integration are enabling multiple chiplets to function together within compact semiconductor packages. Companies developing AI processors, gaming hardware, and cloud computing chips are increasingly investing in advanced interconnect technologies to enhance computing performance while lowering power consumption. For example, several leading semiconductor firms have introduced chiplet-based processors for data center and AI workloads to support higher bandwidth and lower latency requirements. Future demand for high-performance computing and edge AI applications is expected to accelerate adoption of chiplet-enabled advanced packaging solutions globally.

Expansion of Fan-Out Wafer-Level Packaging Technologies

Fan-out wafer-level packaging is witnessing significant adoption across smartphones, wearable devices, automotive electronics, and IoT applications due to its compact design capabilities and superior electrical performance. This technology enables smaller package sizes while improving thermal efficiency and reducing signal loss compared to traditional packaging methods. Consumer electronics manufacturers are increasingly using fan-out packaging for processors, image sensors, and wireless communication chips integrated into lightweight devices. Automotive semiconductor suppliers are also adopting fan-out technologies to support advanced driver assistance systems and electric vehicle control modules. Packaging manufacturers continue to invest in high-density redistribution layers and advanced substrate innovations to improve performance reliability. The future impact of this trend is expected to include broader adoption of ultra-thin semiconductor packages in augmented reality devices, connected healthcare systems, and next-generation communication infrastructure.

Market Drivers

Increasing Demand for High-Performance Consumer Electronics

The rapid growth of smartphones, tablets, gaming devices, wearable electronics, and AI-enabled consumer products is driving strong demand for advanced semiconductor packaging technologies. Modern electronic devices require compact chips with higher processing power, improved thermal performance, and reduced energy consumption. Advanced packaging solutions such as flip-chip, system-in-package, and wafer-level packaging help manufacturers integrate multiple functionalities into smaller device footprints. Consumer electronics companies are increasingly investing in miniaturized semiconductor components to improve product portability and battery efficiency. For instance, high-end smartphone manufacturers continue integrating advanced processors and 5G communication chips that require sophisticated packaging technologies for thermal control and signal optimization. As demand for connected consumer devices continues to increase worldwide, semiconductor packaging companies are expected to expand production capacities and accelerate technological innovation.

Growth of Electric Vehicles and Automotive Electronics

The growing adoption of electric vehicles and intelligent transportation systems is significantly contributing to growth of the advanced packaging market. Modern vehicles utilize advanced semiconductor systems for battery management, infotainment, autonomous driving, power conversion, and safety monitoring applications. Advanced packaging technologies improve durability, thermal resistance, and performance reliability under harsh automotive operating conditions. Automotive manufacturers are increasingly deploying compact semiconductor packages to reduce system size and improve energy efficiency within electric vehicles. For example, advanced driver assistance systems rely heavily on high-performance chips packaged using 2.5D and flip-chip technologies for rapid data processing. Government incentives supporting electric mobility and automotive digitalization are further increasing semiconductor demand globally. Future expansion of autonomous vehicle infrastructure and connected transportation systems is expected to strengthen long-term market growth.

Market Restraint

High Manufacturing Costs and Complex Production Processes

High manufacturing costs and technological complexity remain major restraints affecting the advanced packaging market. Advanced semiconductor packaging technologies require expensive fabrication equipment, precision manufacturing environments, and highly specialized engineering expertise. Processes such as wafer-level packaging, 3D IC integration, and advanced substrate manufacturing involve multiple production stages and stringent quality control standards, increasing operational expenses for manufacturers. Smaller semiconductor companies often face challenges in adopting advanced packaging technologies due to limited capital investment capabilities. Additionally, rising raw material costs and supply chain disruptions can further increase production expenditures. For example, shortages of semiconductor-grade substrates and advanced interconnect materials have impacted production timelines across several regions. The complexity of integrating heterogeneous semiconductor components also increases the risk of manufacturing defects and testing challenges. These factors may limit adoption among cost-sensitive industries and create barriers for new market entrants during the forecast period.

Market Opportunities

Expansion of Artificial Intelligence Infrastructure

The rapid expansion of artificial intelligence infrastructure presents significant opportunities for advanced packaging manufacturers. AI processors require high-bandwidth memory integration, improved thermal management, and low-latency communication systems that can only be achieved through sophisticated packaging architectures. Data centers, cloud computing providers, and AI hardware developers are increasingly investing in 2.5D and 3D packaging technologies to support large-scale AI workloads. Semiconductor companies are also developing chiplet-based AI accelerators using advanced packaging solutions to optimize computing efficiency. Growing deployment of generative AI platforms and machine learning applications is expected to substantially increase semiconductor demand over the next decade. Future opportunities are likely to emerge in edge AI devices, robotics, and industrial automation systems requiring compact and energy-efficient semiconductor packages.

Increasing Investments in Domestic Semiconductor Manufacturing

Governments and private organizations across North America, Europe, and Asia Pacific are increasing investments in domestic semiconductor manufacturing infrastructure, creating strong growth opportunities for advanced packaging providers. National semiconductor development initiatives are encouraging regional supply chain expansion and reducing dependency on imported chip technologies. Advanced packaging facilities are increasingly being integrated into semiconductor manufacturing ecosystems to support local production requirements. For example, several countries are providing financial incentives for semiconductor fabrication plants and packaging research centers focused on AI, automotive, and telecommunications applications. These investments are expected to increase demand for packaging substrates, wafer-level packaging systems, and advanced testing solutions. Future growth opportunities are likely to emerge through regional partnerships, technology transfer programs, and expansion of advanced semiconductor assembly operations worldwide.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 38.7 Billion |

| Market Size in 2026 | USD 41.5 Billion |

| Market Size in 2034 | USD 72.4 Billion |

| CAGR | 7.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Flip-chip packaging dominated the type segment and accounted for 33.6% of the global advanced packaging market share in 2024. The dominance of this segment is primarily attributed to its superior electrical performance, compact design, and high input/output density compared to conventional wire-bond packaging methods. Flip-chip technology is widely adopted across smartphones, graphics processors, gaming consoles, and networking devices due to its ability to support high-speed data transmission and thermal efficiency. Semiconductor manufacturers are increasingly using flip-chip packaging for artificial intelligence accelerators and high-performance computing chips. The growing use of compact semiconductor architectures in wearable devices and automotive electronics has also reinforced segment growth. Several electronics manufacturers are expanding production of flip-chip integrated circuits to support rising demand for miniaturized and energy-efficient electronic products.

Fan-out wafer-level packaging is projected to witness the fastest CAGR of 9.1% during the forecast period. The segment is gaining momentum due to increasing demand for thinner semiconductor packages with enhanced electrical performance and reduced power consumption. Fan-out wafer-level packaging enables higher functionality and improved signal transmission without requiring traditional substrates. The technology is becoming increasingly popular in premium smartphones, AI processors, and advanced automotive electronics. Semiconductor companies are investing heavily in panel-level fan-out packaging technologies to improve production efficiency and lower manufacturing costs. Rising adoption of 5G-enabled devices and edge computing infrastructure is expected to create strong future demand for advanced wafer-level packaging solutions. Increasing integration of multiple chips into compact modules will further accelerate segment expansion through 2034.

By Material

Organic substrates dominated the material segment with a 46.8% share in 2024 owing to their cost-effectiveness, flexibility, and strong compatibility with advanced semiconductor packaging technologies. Organic substrate materials are widely used in flip-chip ball grid array packaging, high-density interconnect systems, and system-in-package applications. The material supports efficient electrical connectivity while reducing package weight and manufacturing complexity. Consumer electronics manufacturers are increasingly adopting organic substrates in smartphones, laptops, and gaming devices due to growing demand for compact semiconductor assemblies. Advancements in substrate design and multilayer integration technologies are also contributing to market growth. Several semiconductor packaging companies are expanding organic substrate manufacturing capacity to meet increasing global demand for high-performance chips and AI processors.

Glass substrate materials are anticipated to register the fastest CAGR of 8.8% during the forecast period. The growth of this segment is associated with increasing demand for higher bandwidth performance, reduced signal loss, and improved thermal stability in advanced semiconductor devices. Glass substrates are gaining attention in next-generation semiconductor packaging because they offer better dimensional stability and fine-line interconnect capabilities. Technology companies are exploring glass substrate integration for artificial intelligence chips, high-performance computing systems, and data center processors. The rising complexity of semiconductor architectures is encouraging manufacturers to adopt materials capable of supporting higher chip density and improved electrical efficiency. Continued research in advanced interposer technologies and heterogeneous integration solutions is expected to drive long-term demand for glass substrate materials.

By End-Use

Consumer electronics dominated the end-use segment and accounted for 39.4% of the advanced packaging market share in 2024. The dominance of this segment is driven by continuous growth in smartphones, tablets, gaming consoles, laptops, and wearable electronics. Advanced packaging technologies are essential for improving device performance, reducing energy consumption, and enabling compact product designs. Semiconductor manufacturers are increasingly integrating advanced packaging into processors, memory chips, and sensors used in consumer electronics devices. Growing consumer demand for AI-enabled smartphones, augmented reality devices, and high-speed computing products continues to support market expansion. Electronics companies are also investing in next-generation chip packaging technologies to improve thermal management and battery efficiency in portable devices.

Automotive electronics is projected to grow at the fastest CAGR of 9.4% during the forecast period due to rapid expansion of electric vehicles, autonomous driving technologies, and advanced driver assistance systems. Modern vehicles require high-performance semiconductor components for battery management, infotainment systems, radar sensors, and vehicle connectivity platforms. Advanced packaging solutions provide improved durability, thermal efficiency, and reliability required for automotive operating environments. Automotive manufacturers are increasingly collaborating with semiconductor companies to develop compact and high-speed packaging technologies suitable for electric mobility applications. Rising deployment of autonomous driving systems and connected vehicle infrastructure is expected to create substantial future opportunities for advanced semiconductor packaging providers worldwide.

Advanced Packaging Market Segmentations

By Type

- Flip-Chip Packaging

- Fan-Out Wafer-Level Packaging

- 2.5D Packaging

- 3D Packaging

- System-in-Package (SiP)

- Embedded Die Packaging

By Material

- Organic Substrates

- Ceramic Substrates

- Glass Substrates

- Leadframes

- Bonding Wires

- Encapsulation Resins

By End-User

- Consumer Electronics

- Automotive Electronics

- Healthcare Devices

- Industrial Automation

- Telecommunications

- Aerospace & Defense

Regional Analysis

North America

North America accounted for 26.8% of the global advanced packaging market share in 2025 and is projected to expand at a CAGR of 7.3% during the forecast period. The region continues to witness strong demand due to increasing investments in semiconductor manufacturing, artificial intelligence infrastructure, and high-performance computing technologies. The United States and Canada are investing heavily in domestic chip production facilities to reduce dependence on overseas semiconductor supply chains. Advanced packaging technologies such as 2.5D packaging, fan-out wafer-level packaging, and system-in-package solutions are gaining traction across consumer electronics and automotive sectors. Rising adoption of electric vehicles and advanced driver assistance systems is also supporting regional market expansion.

The United States remained the dominant country in North America due to strong presence of semiconductor manufacturers, research institutions, and packaging technology providers. One major growth driver is the expansion of AI data centers requiring high-bandwidth memory integration and advanced chip architectures. Several packaging facilities in Arizona, Texas, and California are increasing investments in heterogeneous integration technologies. Consumer electronics companies are also demanding compact and energy-efficient semiconductor packages for smartphones, wearables, and gaming devices. The region is further benefiting from government-backed semiconductor incentive programs and growing collaborations between chipmakers and packaging companies focused on next-generation substrate technologies.

Europe

Europe represented 21.4% of the global advanced packaging market in 2025 and is expected to grow at a CAGR of 6.9% through 2034. The region is witnessing increasing adoption of advanced semiconductor packaging in automotive electronics, industrial automation, aerospace, and medical equipment manufacturing. European countries are emphasizing regional semiconductor independence and strengthening electronics manufacturing capabilities. Demand for advanced packaging is rising due to the rapid deployment of electric mobility infrastructure and Industry 4.0 technologies. Growth in renewable energy systems and smart industrial sensors is also supporting the need for durable and high-performance semiconductor packaging solutions.

Germany dominated the European market owing to its strong automotive electronics and industrial manufacturing ecosystem. A major regional growth factor is the increasing use of advanced semiconductor packaging in electric vehicles and autonomous driving systems. Automotive manufacturers are integrating compact semiconductor modules with higher processing capabilities to support battery management, infotainment, and radar systems. Germany, France, and the Netherlands are also investing in semiconductor research initiatives focused on chip miniaturization and advanced substrate development. Growing deployment of industrial robotics and smart manufacturing equipment across Europe is expected to create long-term demand for reliable and thermally efficient packaging technologies.

Asia Pacific

Asia Pacific dominated the advanced packaging market with a 41.7% share in 2025 and is projected to register a CAGR of 8.4% during the forecast period. The region benefits from strong semiconductor manufacturing infrastructure, rising consumer electronics production, and expanding investments in foundry and packaging facilities. Countries including China, Taiwan, South Korea, and Japan continue to lead global semiconductor assembly and packaging operations. Rapid growth in smartphone manufacturing, cloud computing infrastructure, and 5G deployment is accelerating demand for advanced packaging technologies. The region is also witnessing increasing production of AI processors and high-performance memory chips requiring sophisticated integration techniques.

China emerged as the dominant country in Asia Pacific due to large-scale investments in semiconductor self-sufficiency initiatives and electronics manufacturing expansion. One major growth driver is the rapid increase in domestic semiconductor packaging capacity supported by government incentives and industrial modernization programs. Chinese technology companies are investing heavily in advanced chip packaging to support artificial intelligence servers, telecommunications equipment, and electric vehicles. Taiwan and South Korea are also strengthening regional competitiveness through innovations in wafer-level packaging and 3D stacking technologies. Rising exports of consumer electronics and semiconductor components across Asia Pacific continue to reinforce long-term market growth.

Middle East & Africa

The Middle East & Africa accounted for 4.8% of the global advanced packaging market share in 2025 and is forecast to expand at a CAGR of 6.1% during the forecast period. The region is gradually increasing investments in electronics manufacturing, telecommunications infrastructure, and smart city projects. Demand for advanced semiconductor packaging is rising due to expansion of industrial automation systems, renewable energy projects, and digital transformation initiatives. Governments across the Gulf region are supporting technology diversification strategies aimed at reducing reliance on oil-based economies. Increasing deployment of connected infrastructure and IoT-enabled systems is supporting growth opportunities for semiconductor packaging providers.

Saudi Arabia remained the dominant country in the regional market due to rising investments in smart infrastructure and industrial digitalization programs. A key growth factor is the rapid deployment of data centers and telecommunications networks supporting cloud computing and 5G connectivity. Semiconductor packaging demand is also increasing in industrial monitoring systems, energy management solutions, and defense electronics applications. The United Arab Emirates is expanding electronics assembly activities while African economies are witnessing increasing imports of consumer electronics and connected devices. Growing investment in renewable energy systems and smart transportation infrastructure is expected to create additional demand for advanced packaging technologies across the region.

Latin America

Latin America held 5.3% of the global advanced packaging market in 2025 and is anticipated to grow at the fastest CAGR of 8.7% during the forecast period. The region is benefiting from increasing electronics consumption, rising automotive production, and growing investments in telecommunications infrastructure. Expansion of manufacturing activities in Mexico and Brazil is creating new opportunities for semiconductor assembly and packaging operations. Demand for advanced packaging technologies is also rising in industrial automation, consumer electronics, and medical device applications. Increasing adoption of connected devices and digital payment systems is contributing to regional market growth.

Brazil dominated the Latin American market due to rising industrial electronics production and expanding automotive manufacturing activities. One unique growth driver is the increasing localization of consumer electronics assembly operations aimed at reducing import dependence. Brazilian manufacturers are integrating advanced semiconductor components into automotive systems, household appliances, and telecommunications equipment. Mexico is also strengthening its semiconductor supply chain integration through partnerships with North American electronics manufacturers. Rising demand for affordable smartphones, connected industrial equipment, and cloud-based infrastructure solutions is expected to support continued expansion of advanced packaging technologies across Latin America.

Competitive Landscape

The advanced packaging market is characterized by strong competition among semiconductor manufacturers, outsourced semiconductor assembly and test providers, substrate suppliers, and integrated device manufacturers. Companies are increasingly investing in heterogeneous integration, wafer-level packaging, 2.5D and 3D packaging technologies, and chiplet-based architectures to improve processing performance and energy efficiency. Strategic partnerships between foundries and packaging technology providers are becoming common as demand for AI processors, high-performance computing chips, and automotive electronics accelerates globally.

Taiwan Semiconductor Manufacturing Company (TSMC) remained the leading player in the advanced packaging market due to its extensive portfolio of CoWoS, InFO, and SoIC packaging technologies. The company continues to expand packaging capacity to support rising demand for artificial intelligence accelerators and advanced computing processors. Intel Corporation is investing heavily in Foveros and EMIB packaging technologies to strengthen its semiconductor manufacturing ecosystem and support next-generation data center applications.

Samsung Electronics is focusing on advanced memory packaging and heterogeneous integration technologies for AI and mobile processors. ASE Technology Holding is expanding advanced packaging and testing facilities across Asia to address increasing demand for high-density semiconductor packages. Amkor Technology continues to strengthen its automotive and industrial semiconductor packaging portfolio through strategic collaborations and capacity expansion initiatives. Several companies are also investing in substrate innovation, thermal management materials, and panel-level packaging technologies to improve manufacturing scalability and reduce operational costs.

Key Players List

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Intel Corporation

- Samsung Electronics Co., Ltd.

- ASE Technology Holding Co., Ltd.

- Amkor Technology, Inc.

- JCET Group Co., Ltd.

- Powertech Technology Inc.

- Texas Instruments Incorporated

- Advanced Micro Devices, Inc.

- Qualcomm Technologies, Inc.

- Broadcom Inc.

- Micron Technology, Inc.

- NVIDIA Corporation

- SK Hynix Inc.

- IBM Corporation

- Infineon Technologies AG

- STMicroelectronics N.V.

- Fujitsu Limited

- Renesas Electronics Corporation

- Deca Technologies Inc.