3D Ic And 25D Ic Packaging Market Size and Growth

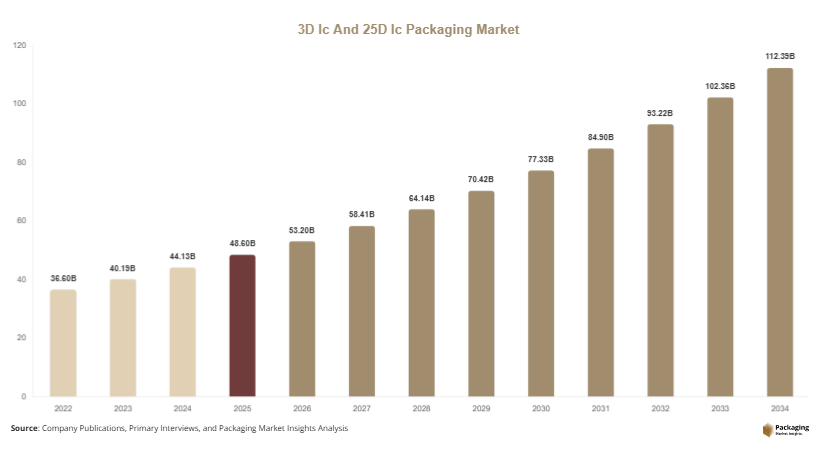

The global 3D Ic And 25D Ic packaging market was valued at approximately USD 48.6 billion in 2025 and is projected to reach USD 53.2 billion in 2026, reflecting a steady increase in adoption of advanced packaging technologies. By 2034, the market is expected to reach USD 112.4 billion, expanding at a CAGR of 9.8% from 2025 to 2034. This growth trajectory highlights the rising importance of packaging innovation in addressing performance limitations of traditional semiconductor scaling. The global 3D Ic And 25D Ic packaging market is experiencing sustained growth due to increasing demand for advanced semiconductor integration across high-performance computing, consumer electronics, and automotive applications.

One of the key growth factors is the rising deployment of artificial intelligence and machine learning workloads, which require faster data transfer and lower latency. Advanced packaging technologies such as 3D IC and 2.5D IC provide improved bandwidth and efficiency, making them essential for modern computing systems. Another important factor is the growing demand for compact and energy-efficient consumer electronics. Devices such as smartphones, wearables, and tablets require higher integration density, which is effectively supported by advanced packaging solutions. Additionally, the expansion of cloud computing and data centers is further boosting demand for high-performance chips, driving adoption of these technologies.

Key Highlights:

- Asia Pacific dominated the market with a 39.1% share in 2025, while Latin America is projected to grow at the fastest CAGR of 10.4%.

- 2.5D IC packaging led the type segment with a 57.8% share, while 3D IC packaging is expected to grow at a CAGR of 11.2%.

- Interposer-based packaging dominated with a 49.3% share, while fan-out wafer-level packaging is forecasted to grow at a CAGR of 10.7%.

- Consumer electronics applications led the segment with 44.6% share, while automotive electronics is expected to grow at a CAGR of 10.9%.

- China remained the dominant country with a market size of USD 14.3 billion in 2025 and USD 15.8 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Heterogeneous Integration

The market is undergoing a structural shift toward heterogeneous integration, where multiple semiconductor components are combined into a single package to enhance functionality and efficiency. This approach is gaining traction as traditional transistor scaling becomes more challenging and costly. 2.5D IC packaging, in particular, enables integration of logic, memory, and analog components using interposers, resulting in improved performance and lower power consumption. The flexibility offered by heterogeneous integration allows manufacturers to customize chip architectures according to specific application requirements. As industries demand higher computing capabilities, this trend is expected to strengthen and play a critical role in shaping future semiconductor design strategies.

Expansion of AI and Data-Centric Workloads

The rapid growth of artificial intelligence and data-driven applications is significantly influencing the demand for advanced packaging technologies. AI workloads require high bandwidth memory and fast communication between processing units, which can be effectively achieved through 3D IC and 2.5D IC packaging. These technologies enable closer integration of components, reducing latency and improving computational efficiency. Data centers and cloud service providers are increasingly adopting these solutions to manage large-scale workloads and improve energy efficiency. Additionally, the rise of edge computing is driving demand for compact and high-performance semiconductor solutions, further reinforcing the importance of advanced IC packaging technologies in modern computing environments.

Market Drivers

Rising Demand for High-Performance Computing Systems

The growing need for high-performance computing systems is a major factor driving the 3D Ic And 25D Ic packaging market. Applications such as scientific research, financial modeling, and AI processing require high-speed data transfer and efficient thermal management. Traditional packaging methods are often unable to meet these requirements, leading to increased adoption of advanced packaging solutions. 3D IC packaging enables vertical stacking of chips, reducing interconnect length and improving performance. Meanwhile, 2.5D IC packaging offers a balance between cost and performance, making it suitable for a wide range of applications. This increasing reliance on HPC systems is expected to continue driving market growth.

Expansion of Consumer Electronics and IoT Ecosystem

The proliferation of consumer electronics and IoT devices is another key factor contributing to market growth. Devices such as smartphones, wearables, and smart home systems require compact and energy-efficient semiconductor components. Advanced packaging technologies allow higher integration density and improved functionality within smaller footprints. Additionally, IoT applications demand low power consumption and reliable performance, which can be achieved through advanced IC packaging. As the number of connected devices continues to rise globally, the demand for efficient packaging solutions is expected to grow significantly.

Market Restraint

High Manufacturing Complexity and Cost Challenges

The adoption of advanced IC packaging technologies is limited by high manufacturing complexity and associated costs. The production of 3D IC and 2.5D IC packages involves intricate processes such as through-silicon vias, wafer bonding, and interposer integration. These processes require specialized equipment and expertise, increasing overall production costs. Furthermore, yield challenges and thermal management issues add to the complexity, making it difficult for manufacturers to maintain profitability. For instance, defects in stacked dies can lead to failure of the entire package, resulting in higher material waste and operational inefficiencies. These challenges are particularly significant in cost-sensitive markets, where traditional packaging methods may still be preferred.

Market Opportunities

Growing Role of Automotive Electronics and Electrification

The automotive industry is emerging as a strong growth avenue for the 3D Ic And 25D Ic packaging market. Electric vehicles and advanced driver-assistance systems rely heavily on semiconductor components for efficient operation. Advanced packaging technologies provide improved performance, reliability, and thermal management, which are essential for automotive applications. As the industry moves toward electrification and automation, the demand for high-performance semiconductor packaging is expected to increase. This trend presents significant opportunities for market players to expand their presence in the automotive sector.

Expansion of Semiconductor Ecosystems in Emerging Markets

Emerging economies are investing heavily in semiconductor manufacturing to strengthen domestic capabilities and reduce reliance on imports. Governments are offering incentives and policy support to attract investments in chip fabrication and packaging facilities. This expansion is expected to boost demand for advanced packaging technologies, including 3D IC and 2.5D IC solutions. Countries in Asia and Latin America are particularly active in developing semiconductor ecosystems, providing cost advantages and skilled labor. As new facilities become operational, the adoption of advanced packaging technologies is likely to accelerate, creating substantial growth opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 48.6 Billion |

| Market Size in 2026 | USD 53.2 Billion |

| Market Size in 2034 | USD 112.4 Billion |

| CAGR | 9.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

The 2.5D IC packaging segment held the largest share of the market in 2024, accounting for approximately 57.8% of total revenue. This dominance is attributed to its ability to deliver high performance while maintaining relatively lower manufacturing complexity compared to full 3D IC packaging. The use of interposers allows efficient integration of multiple dies, improving signal integrity and reducing power consumption. These advantages make 2.5D IC packaging a preferred choice for high-performance computing applications, including graphics processing units and data center processors. Its widespread adoption is expected to continue due to its balance of cost and performance benefits.

The 3D IC packaging segment is anticipated to grow at the fastest CAGR of 11.2% during the forecast period. This growth is driven by increasing demand for higher integration density and improved performance. 3D IC packaging involves vertical stacking of semiconductor dies, enabling shorter interconnects and faster data transfer. The technology is particularly suitable for applications such as artificial intelligence and machine learning, where performance and efficiency are critical. Continuous advancements in through-silicon via technology are also improving manufacturing efficiency, supporting the growth of this segment.

By Technology

Interposer-based packaging dominated the market in 2024 with a share of approximately 49.3%. This technology is widely used in 2.5D IC packaging and provides a reliable platform for integrating multiple semiconductor dies. It offers improved signal integrity and reduced power consumption, making it suitable for high-performance applications. The widespread adoption of interposer-based solutions in data centers and advanced computing systems contributes to its strong market position.

Fan-out wafer-level packaging is expected to grow at a CAGR of 10.7% over the forecast period. This technology eliminates the need for a substrate, resulting in thinner and more compact packages. It is increasingly used in consumer electronics due to its cost efficiency and performance benefits. The growing demand for miniaturized devices and continuous advancements in packaging technologies are driving the adoption of fan-out wafer-level packaging, making it a key growth segment.

By Application

Consumer electronics accounted for the largest share of the market in 2024, contributing approximately 44.6% of total revenue. The increasing use of smartphones, tablets, and wearable devices drives demand for advanced IC packaging solutions. These applications require compact and energy-efficient components, which can be achieved through 3D and 2.5D IC packaging technologies. Continuous innovation in consumer electronics further supports segment growth.

Automotive electronics is projected to be the fastest-growing segment, with a CAGR of 10.9% during the forecast period. The increasing adoption of electric vehicles and advanced safety systems is driving demand for high-performance semiconductor components. Advanced packaging technologies provide improved reliability and thermal management, which are essential for automotive applications. This growth is further supported by the rising focus on autonomous driving technologies.

3D Ic And 25D Ic Packaging Market Segmentations

By Type

- 3D IC Packaging

- 2.5D IC Packaging

By Technology

- Interposer-Based Packaging

- Fan-Out Wafer-Level Packaging

- Through-Silicon Via (TSV)

By Application

- Consumer Electronics

- Automotive Electronics

- IT & Telecommunications

- Industrial

Regional Analysis

North America

North America accounted for approximately 24.7% of the global 3D Ic And 25D Ic packaging market in 2025 and is projected to grow at a CAGR of 8.9% through 2034. The region benefits from a strong technological ecosystem, including leading semiconductor companies and advanced research institutions. Continuous investments in innovation and high demand for advanced computing solutions are driving market growth. The presence of established infrastructure and early adoption of new technologies further support expansion across the region.

The United States remains the dominant country in North America, driven by its robust semiconductor industry and focus on innovation. A unique growth factor is the increasing deployment of artificial intelligence and cloud computing infrastructure. These technologies require advanced packaging solutions to enhance performance and efficiency, thereby boosting market demand in the region.

Europe

Europe held a market share of around 18.6% in 2025 and is expected to grow at a CAGR of 8.5% during the forecast period. The region’s growth is supported by its strong industrial base and increasing adoption of digital technologies. Demand for advanced semiconductor packaging is rising across automotive, industrial, and telecommunications sectors. Additionally, investments in research and development are contributing to the advancement of packaging technologies.

Germany dominates the European market, primarily due to its well-established automotive industry. A unique growth factor in this region is the rapid adoption of electric vehicles, which require reliable semiconductor components. Advanced packaging technologies enable better performance and thermal management, supporting the growing demand from the automotive sector.

Asia Pacific

Asia Pacific led the global market with a 39.1% share in 2025 and is projected to grow at a CAGR of 10.6% through 2034. The region’s dominance is attributed to the presence of major semiconductor manufacturing hubs and strong demand for consumer electronics. Countries such as China, South Korea, and Taiwan play a critical role in driving market growth through large-scale production and technological advancements.

China is the dominant country in the region, supported by significant government investments in semiconductor infrastructure. A unique growth factor is the rapid expansion of domestic chip production capabilities, which increases demand for advanced packaging technologies. This expansion is expected to strengthen the region’s position in the global market.

Middle East & Africa

The Middle East & Africa region accounted for approximately 7.3% of the market in 2025 and is expected to grow at a CAGR of 9.1% over the forecast period. The region is gradually adopting advanced technologies, supported by investments in digital infrastructure and smart city initiatives. Increasing awareness of semiconductor applications is also contributing to market growth.

The United Arab Emirates is a key contributor to the regional market. A unique growth factor is the focus on economic diversification through technology-driven initiatives. These efforts are encouraging the adoption of advanced semiconductor solutions, including IC packaging technologies, thereby supporting market expansion.

Latin America

Latin America held a market share of 10.3% in 2025 and is projected to grow at the fastest CAGR of 10.4% during the forecast period. The region is witnessing increased adoption of semiconductor technologies across various industries, including consumer electronics and automotive. Growing industrialization and technological advancements are supporting market growth.

Brazil dominates the Latin American market due to its expanding industrial base and increasing adoption of advanced technologies. A unique growth factor is the growth of local electronics manufacturing, which drives demand for advanced IC packaging solutions. This trend is expected to continue, contributing to regional market expansion.

Competitive Landscape

The 3D Ic And 25D Ic packaging market is characterized by moderate competition, with several global players focusing on technological innovation and strategic collaborations. Companies are investing heavily in research and development to enhance packaging efficiency and performance. The market is also witnessing partnerships between semiconductor manufacturers and technology providers to expand capabilities and meet growing demand.

Intel Corporation is a leading player in the market, known for its strong focus on advanced packaging technologies. The company has recently introduced new packaging architectures aimed at improving chip performance and integration capabilities. Other key players are also expanding their manufacturing capacities and developing innovative solutions to strengthen their market positions and address evolving industry requirements.

Key Players List

- Intel Corporation

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Samsung Electronics Co., Ltd.

- ASE Technology Holding Co., Ltd.

- Amkor Technology, Inc.

- Broadcom Inc.

- Qualcomm Incorporated

- NVIDIA Corporation

- Advanced Micro Devices (AMD)

- Micron Technology, Inc.

- Texas Instruments Incorporated

- STMicroelectronics

- Infineon Technologies AG

- Powertech Technology Inc.

- JCET Group Co., Ltd.